Mortgages can be confusing, largely due to the sheer number of new terms and jargon that might confuse borrowers. Terms like ‘LIBOR’ and ‘APRC’ are not commonly used outside the context of mortgages and finance, so many borrowers are unfamiliar with them.

Currently there are 10.94 million mortgages in the UK, and the numbers continue to rise. This shows the extreme importance that mortgages have on the UK housing market. However, many borrowers may feel put off by confusing terminology used by lenders. In this glossary, we will explain all the key mortgage terms you will need in order to make an informed decision about your home loan.

Mortgage Terms

APRC (Annual Percentage Rate of Charge)

The Annual Percentage Rate of Charge, commonly known as APRC, represents the total cost of credit to a consumer, expressed as an annual percentage of the total amount of credit. It includes the interest rate and other costs associated with the mortgage, such as fees and charges.

AVM (Automated Valuation Model)

AVM stands for Automated Valuation Model, a tool used by some lenders to determine the value of a property based on recent local sales and value trends. It provides an instant valuation without the need for a physical surveyor visit.

Base Rate

The Base Rate is the core interest rate set by the Bank of England. Lenders typically adjust their Standard Variable Rate (SVR) based on changes in the Base Rate.

Bonding Scheme

A Bonding Scheme is an agreement among professionals or tradespeople. It intends to establish a central compensation fund to protect consumers in case of fraud or insolvency.

Buildings Insurance

Buildings Insurance is a type of insurance that protects the property itself against damage or destruction. It may also be combined with contents insurance in a single policy.

Business Buy to Let

Business Buy to Let refers to buying a property for investment purposes. The income is generated from rental payments, and the property’s value may appreciate over time.

Capital and Interest Mortgage

A Capital and Interest mortgage, also known as a repayment mortgage, involves paying both the interest and a portion of the principal amount each month. This gradually reduces the outstanding mortgage balance.

Capped Rate

A Capped Rate mortgage limits the interest rate from rising above a specified level for a set period. This provides some protection against interest rate fluctuations.

Cashback

Cashback is a cash amount paid by a mortgage lender to a customer. This is typically at the beginning of the mortgage contract, as an incentive to choose their mortgage product.

Completion

Completion is the final stage of the house-buying process, occurring after the exchange of contracts. It is when the seller receives the full sale price, and ownership of the property is transferred to the buyer.

Compulsories

Compulsories refer to compulsory insurances that certain lenders may require borrowers to take out, such as buildings insurance.

Consumer Buy to Let

Consumer Buy to Let mortgages are designed for borrowers who did not initially plan to buy for investment purposes, do not own other buy-to-let properties and are only seeking a remortgage.

Contents Insurance

Contents Insurance protects the personal belongings inside the property. In rental properties, the landlord typically insures their belongings, while tenants insure their possessions.

Conveyancing

Conveyancing is the legal process of transferring property ownership from seller to buyer. It includes searches, title checks and handling the legal paperwork.

Council Tax

Council Tax is a local authority charge based on the value of a property. Tenants in rented or buy-to-let accommodation are usually responsible for paying this tax.

County Court Judgment (CCJ)

A County Court Judgment is a ruling issued against a person who has defaulted on a debt. It can affect creditworthiness and may lead to higher interest rates or loan denials.

Credit Reference Agency

Credit Reference Agencies hold credit records containing information about an individual’s financial history. Lenders use these records to assess creditworthiness.

Current Account

A Current Account is a bank account linked to a chequebook and/or debit card. It offers instant access to funds but usually little or no interest on the balance.

Deeds

Deeds are formal written documents. They prove property ownership and enable the transfer of a property from seller to buyer.

Decree

A Decree is the Scottish version of a County Court Judgement (CCJ).

Deposit

The Deposit is the initial lump sum payment made by the buyer towards the total purchase price of the property. It is commonly around 5% to 10% of the property’s value.

Deposit-based Savings

Deposit-based Savings provide regular interest based on the amount invested, offering a predictable return compared to riskier investments.

Discounted Rate

A Discounted Rate mortgage offers an interest rate lower than the lender’s Standard Variable Rate (SVR) for a specific period.

Distance Mortgage Mediation Contract

Distance Mortgage Mediation Contract refers to mortgages completed remotely, without face-to-face interactions.

Diversification

Diversification is the practice of spreading investments across various asset classes to reduce risk.

Durable Medium

A Durable Medium is a document capable of being stored and accessed for future reference, often used for mortgage agreements.

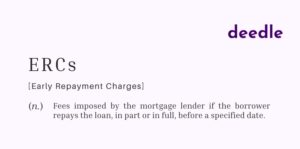

Early Repayment Charges (ERCs)

Early Repayment Charges are fees imposed by the mortgage lender if the borrower repays the loan, in part or in full, before a specified date.

Employment Status

Employment Status refers to a borrower’s working arrangements, affecting mortgage eligibility.

Endowment Mortgage

An Endowment Mortgage involves repaying only the interest on the mortgage while simultaneously investing in an endowment policy to repay the capital at the end of the term.

Exchange of Contracts

The Exchange of Contracts makes the property purchase legally binding for both the buyer and seller.

Execution-only/Non-advice

Execution-only or Non-advice services do not provide guidance or advice, only carrying out the customer’s instructions.

Fixed Rate

A Fixed-Rate mortgage locks in the interest rate for a specified period, providing payment stability.

Flexible Mortgage

A Flexible Mortgage allows borrowers to make overpayments, underpayments or take payment holidays.

Graduate Mortgage

A Graduate Mortgage is tailored for recent graduates with unique features, such as lower deposit requirements.

Gross

Gross refers to income or interest earned before tax or deductions.

Growth

A Growth strategy aims to maximise capital value without a requirement for generating income.

Higher Lending Charge

The Higher Lending Charge is an insurance premium required by some lenders when the loan-to-value ratio exceeds a certain level.

Home and Contents Insurance

Home and Contents Insurance combines buildings and contents cover into a single policy.

Illustration

An Illustration is a lender’s estimate of monthly payments and associated costs for a specific mortgage.

Impaired Credit

Impaired Credit mortgages cater to borrowers with credit problems who do not qualify for standard mortgage products.

Income

An Income strategy aims to achieve a minimum level of income from an investment to fund everyday expenses.

Independent Mortgage Advice

Independent Mortgage Advice refers to advice provided by professionals who have access to the entire mortgage market. They do not accept any commission from lenders, eliminating potential conflicts of interest.

Interest

Interest is the amount charged by a lender on the borrowed money, representing the cost of borrowing.

Interest-Only Mortgage

An Interest-Only Mortgage involves paying only the interest on the loan for a specified period. The capital is to be repaid at the end of the term through other means.

ISA Mortgage

An ISA Mortgage is funded by contributions to an Individual Savings Account (ISA). This aims to repay the loan’s capital at the end of the term while the interest is paid separately.

Letting Agent

A Letting Agent helps landlords find suitable properties to buy and manages the rental process, including finding tenants and handling rental agreements.

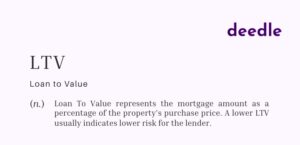

Loan To Value (LTV)

Loan To Value represents the mortgage amount as a percentage of the property’s purchase price. A lower LTV usually indicates lower risk for the lender.

Local Search

A Local Search is an examination of local planning records to identify any upcoming developments or restrictions that may impact the property’s value.

London Inter-Bank Offered Rate (LIBOR)

LIBOR is the interest rate at which leading banks lend to one another. It is sometimes used as a benchmark for certain tracker mortgages.

Mortgage Adviser

A Mortgage Adviser provides guidance on mortgage options. They help borrowers find suitable mortgage products.

Mortgage Refinancing

Mortgage Refinancing involves replacing an existing mortgage with a new one. This is typically to obtain better terms or consolidate other debts.

Mortgage Term

The Mortgage Term is the entire lifespan of the mortgage, indicating the time frame within which it needs to be repaid.

Net

Net refers to income or interest earned after tax or deductions.

Non-Status Loan

A Non-Status Loan is where a borrower’s income is not disclosed during the mortgage application.

Offset Mortgages

Offset Mortgages link the borrower’s savings to their mortgage, reducing the interest paid on the mortgage by offsetting the savings against the outstanding balance.

Overpayment

An Overpayment is a mortgage repayment that exceeds the minimum required, reducing the outstanding balance and potentially shortening the mortgage term.

Payment Holiday

A Payment Holiday allows borrowers to temporarily suspend mortgage repayments. This is particularly beneficial for those with irregular income.

Pension Mortgage

A Pension Mortgage involves using a personal pension to repay the mortgage’s capital at the end of the term.

Premium

A Premium is the regular sum paid for insurance coverage.

Procurement Fee

A Procurement Fee is the amount paid by the mortgage lender to a mortgage adviser/intermediary for providing mortgage applications.

Remortgaging

Remortgaging refers to the process of switching from one mortgage deal to another, either with the same lender or a different one, often to get a better interest rate or terms.

Repayment Vehicle

A Repayment Vehicle is the method used to accumulate funds to repay the capital portion of an interest-only mortgage, such as an endowment policy or ISA.

Search

A Search, also known as a Local Authority Search, involves checking local planning records for any developments or restrictions that may affect the property’s value or use.

Secured Loan

A Secured Loan is a loan that uses the property as collateral, which means the lender can repossess the property if the borrower defaults on payments.

Self-Certification Mortgage

A Self-Certification Mortgage, also known as a self-cert mortgage, is designed for self-employed individuals who may have difficulty proving their income using traditional methods.

Stamp Duty

Stamp Duty, or Stamp Duty Land Tax (SDLT), is a tax imposed by the government on property purchases over a certain threshold.

Status

Status refers to a borrower’s credit record and employment situation, which lenders use to assess creditworthiness.

Standard Variable Rate (SVR)

The Standard Variable Rate is the default interest rate charged by a mortgage lender after the initial fixed or discounted rate period ends.

Surrender

Surrendering an insurance policy, such as an endowment policy, means cashing it in before its maturity date, often resulting in a lower return.

Survey

A Survey is an expert examination of the property to assess its condition and identify any structural issues or repairs needed.

Tracker

A Tracker Mortgage has an interest rate that follows a specified benchmark, such as the Bank of England Base Rate, with the rate fluctuating as the benchmark changes.

Underpayment

An Underpayment is a mortgage repayment that is less than the regular agreed amount, often allowed with flexible mortgages for borrowers with irregular income.